Go paper-free

Amend paper-free preferences for your statements and correspondence.

Explore helpful guides covering everything from credit card basics to account management tips.

If you’ve forgotten your card PIN, get a secure reminder in the app.

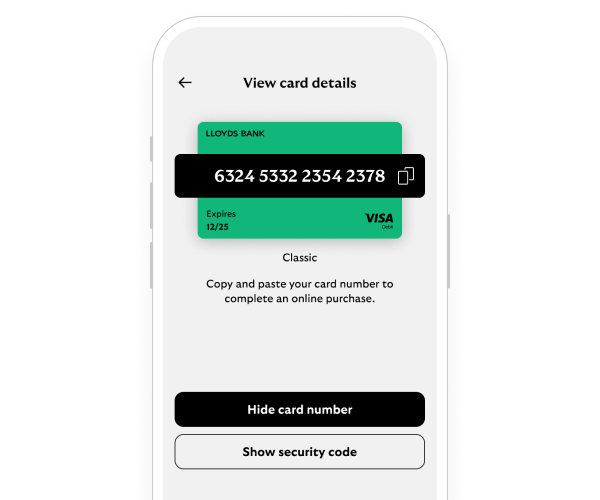

Handy if you need to make purchases when you don’t have your physical card to hand.

Need help?

If you're registered for online banking, the fastest way to get in touch is by messaging us securely online.