The 3 buckets savings formula

We’ve got some tips to help you keep your finances on track. Try our three-bucket formula for success to keep you living your best life.

Savings made easy

- Short-term goal.

- Mid/long-term goal.

- Long-term goal.

We see short-term as less than 5 years, mid/long-term as 5 to 10 years and long-term as 10 years plus.

You can take control, and we can help.

Oh hello good times. The future wants a word

Your 30s and 40s can feel like a financial juggling act. Whether you’re paying off your mortgage or student loan, growing your family, or looking to save and invest for future financial security. We’ve got some tips to help you keep your finances on track. Try our three-bucket formula for success to keep you living your best life.

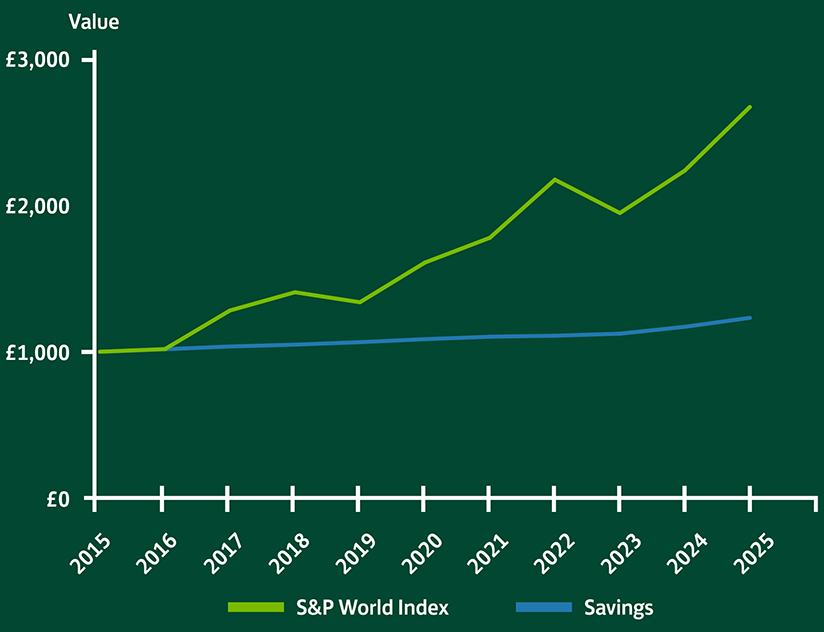

Investment's 10-year track record:

This graph shows a comparison of savings and investments over 10 years.

If you’d invested £1,000 in a fund tracking the S&P World Index (it tracks medium to large companies across 24 developed markets) in 2015, it would have been worth £2,659 in January 2025. Whereas £1,000 kept in a typical savings account would be worth £1,229 in January 2025.

Source:

(Savings) MoneyFacts, 12m Fixed Non-ISA rates, January 2025.

(Investments) S&P Dow Jones Indices, S&P World Index (GBP). Excludes fees. Past performance is not a reliable indicator of future performance. You can see a breakdown of these figures here.

Past performance is not a reliable indicator of future performance. Please remember that the value of investments and the income from them can fall as well as rise, and you may get back less than you invest. If you’re not sure about investing, seek financial advice. There will normally be a charge for that advice.

How to achieve the retirement you want, if you started pension contributions now

|

Age |

25 |

30 |

35 |

40 |

45 |

50 |

|---|---|---|---|---|---|---|

|

Age Monthly pension contributions required for minimum £14,400 a year in retirement |

25 £110 |

30 £135 |

35 £165 |

40 £205 |

45 £265 |

50 £360 |

|

Age Monthly pension contributions required for minimum £31,300 a year in retirement |

25 £750 |

30 £900 |

35 £1,115 |

40 £1,405 |

45 £1,805 |

50 £2,450 |

|

Age Monthly pension contributions required for minimum £43,400 a year in retirement |

25 £1,200 |

30 £1,450 |

35 £1,800 |

40 £2,225 |

45 £2,880 |

50 £3,915 |

-

State Pension

We've assumed you could receive a full state pension entitlement of £11,502 per year if at the qualifying age. We remove this from the calculation if you are under the qualifying age.

You can get a personal State Pension Forecast here.

Income Tax

We've used a basic English income tax calculation, which assumes you will not receive any additional income at retirement.

Tax treatment depends on your individual circumstances.

Your circumstances and tax rules may change in the future.Contributions

The tool assumes that contributions will be made every year including the year of retirement, with monthly contributions annualised for calculation purposes. With the results showing any contributions ceasing before age 75.

Growth Rate

We've assumed a growth rate of 5% per year to your pension value, annualised for calculation purposes.

Inflation

We've assumed a 2% inflation rate in line with current FCA guidance, annualised for calculation purposes.

Charges

We've assumed a charge of 0.7% per year, annualised for calculation purposes.

Tax-Free Lump Sum

We've assumed that a 25% tax-free lump sum will be taken out of your pension, and the full amount of projected pension will be taken as income. However, it is possible to amend this percentage.

Retirement Living Standards

We use estimations from the PLSA/Loughborough University Retirement Living Standards for a single person.

Withdrawal rate

We've assumed that you are taking a guaranteed income for life, also known as an annuity at 4% per year of the projected funds. This will be after any tax-free cash up to 25% has been taken.

Pension allowances

We've not assumed any tax charges from exceeding allowances such as the annual allowance or money purchase annual allowance.

Net and Gross Figures

All of the figures we provide are net (i.e. after deduction of income tax) except for the gross monthly pension contribution figure.

Important information – This article isn’t personal advice. If you’d like to discuss any of the topics covered here, including the actions for your individual circumstances, please contact your financial adviser. If you do not have a financial adviser, you may be able to access one with Lloyds Wealth (fees and eligibility criteria apply). Unbiased is a service that finds a local adviser based on your requirements. You can also find mortgage brokers, accountants, and solicitors on Unbiased.

The contents of this page are accurate as of 10/01/2025. Our views and references to pensions, tax, investment, or their rules, may have changed since then.