Managing Your Mortgage

Learn how to make the best of your mortgage with us

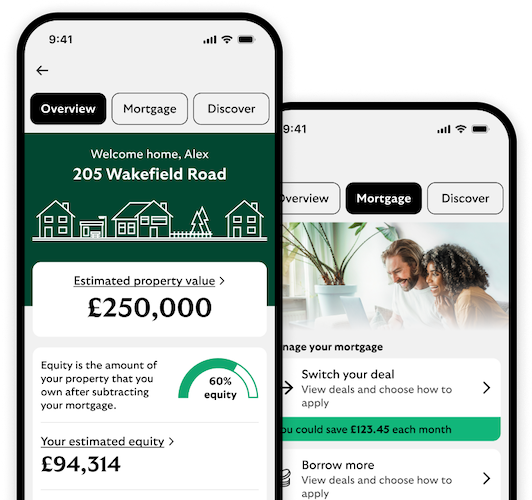

Your mortgage made simple with HomeWise

Manage your mortgage easily online or in the app

- View estimated property value and equity.

- View your personalised rates and apply to switch to a new deal.

- Help save you money on your utility bills.

You may also like