Help and guidance

Need help with our products and services? You're in the right place.

How to message us Help and support person carefully holding three tiers of delicate china in their handsLet's get you there

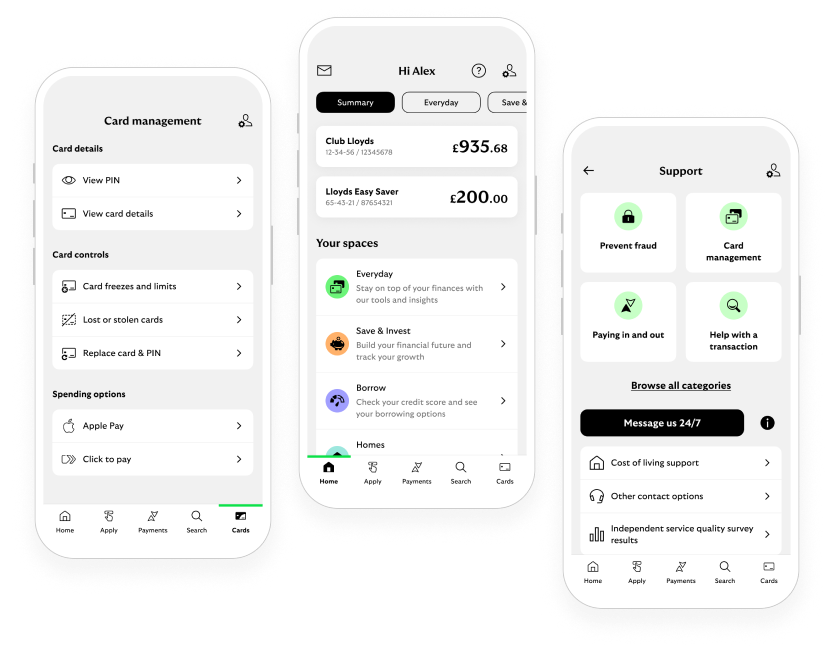

Help with everyday banking

Making banking easier

Lloyds is proud to be part of the same family as Halifax and Bank of Scotland. We’re introducing more ways you can manage any personal accounts you have with Lloyds, Halifax or Bank of Scotland in one place, using co-servicing. Whether that’s online through the apps and online banking, or with a colleague over the phone, or in a branch.

You may also like

Service status

Learn about any planned work we’ve got coming up and what it might mean for you.

Legal information

Read up on our legal information and get access to our account terms and conditions.