2025 Budget update

Changes to ISAs from 06 April 2027

The government announced changes to Individual Savings Accounts (ISAs) in the 2025 Budget. These come into effect from 06 April 2027.

Until 06 April 2027 everyone is able to split their £20,000 ISA allowance between the available ISA types in line with the current rules.

From 06 April 2027, your overall £20,000 ISA allowance remains the same. If you’re under 65, there are new rules for cash ISAs.

Cash ISA changes

Stocks and Shares ISA updates

The allowance stays at £20,000

The overall allowance across all ISA types stays at £20,000, so you can choose to put all of this into a Stocks and Shares ISA.

Understanding the ISA changes

What does this mean for you?

The basics of good financial planning don’t change:

- Cash savings are great for short-term goals.

- Considering investing may help your money grow over time.

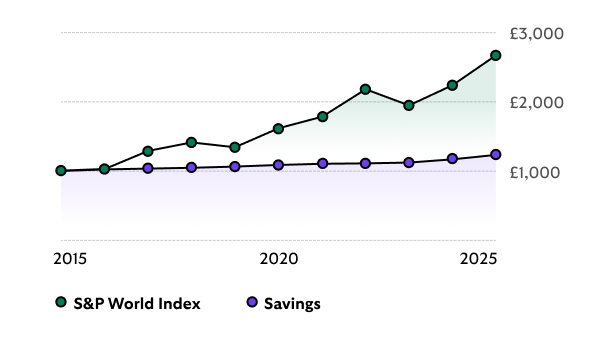

Watch your money work

While future performance isn’t guaranteed, it’s still interesting to compare cash savings performance with investment growth over a 10-year period.

Sources

Savings - MoneyFacts, 12m Fixed Non-ISA rates, January 2025.

Investments - S&P Dow Jones Indices, S&P World Index (GBP). Excludes fees and does not include any dividends or reinvestment.

These figures refer to the past and past performance is not a reliable indicator of future performance. See a data breakdown of the performance in the table here.

Smart strategies for building wealth

Investing in your future

If you want to use your full ISA allowance from 06 April 2027, we’ve got options to help:

- Ready-Made Investment ISA – built and managed by our experts. With low, medium or high-risk investment options, we do the hard work for you.

- Share Dealing ISA – perfect for choosing your own stocks and shares, funds, ETFs and more.

- Invest Wise ISA – free investing account for 18-25 year olds with no admin fee until you’re 26.

New to investing? Start small – you can invest from £50 a month with our Ready-Made Investment ISA. Or set up a regular plan with no trading fees on our Share Dealing ISA.

Thinking about ISA transfers?

Transfers keep your ISA tax benefits – but make sure you do it properly. Don’t take out the money into a normal account during the process. We can help with transfers.

If you’re considering moving money between Cash and Stocks and Shares ISAs, check if it’s right for your goals. Cash is lower risk, but inflation can eat into its buying power. Investments can potentially offer more growth if you’ve got time on your side.

Investing for longer increases the likelihood of positive returns. Over a period of 5 years or more, investments usually give you a higher return compared to cash savings. But investments can go down as well as up in value, so you could get back less than you put in. Tax treatment depends on individual circumstances and may be subject to change in the future.

Protecting your money

The Financial Services Compensation Scheme (FSCS) protects the eligible money you hold with us.

You may also like

ISAs explained

Everything you need to know about ISA’s.

ISA allowances

Current limits for all ISA types.

Savings or investments or both?

Find the right mix for you.

Important legal information

The Lloyds Bank Direct Investments Service is operated by Halifax Share Dealing Limited. Registered Office: Trinity Road, Halifax, West Yorkshire, HX1 2RG. Registered in England and Wales no. 3195646. Halifax Share Dealing Limited is authorised and regulated by the Financial Conduct Authority under registration number 183332. A Member of the London Stock Exchange and an HM Revenue & Customs Approved ISA Manager.