Pensions explained

Pensions can be confusing, so we’ll take you through how they work, the different types, and the benefits having one could bring to your future.

The different types of pension

There are three main types of pensions.

Personal pensions and Self-Invested Personal Pensions (SIPPs)

These are set up by yourself. You decide on the provider, and the amount and frequency of any contributions. Personal contributions will usually benefit from tax relief.

With most personal pensions, you’ll be offered one or more packaged investment solutions, designed to meet your needs at retirement. A SIPP gives you more control on your investments, with a wide range of assets to choose from.

The options you have for taking out your money at retirement depends on the type of pension you have.

Find out more about the personal pensions we offer.

This may be for you if you want to save for retirement and don’t want the hassle of managing it yourself.

Self-Invested Personal Pension (SIPP)

This may be for you if you are confident to make your own investment choices in saving for retirement.

Workplace pensions

Workplace pensions are set up automatically by your employer when you start working for them – this is called auto-enrolment. Usually, when you pay into this pension from your salary, your employer does too.

There are two types of Workplace pensions:

- Defined contribution – Contributions from you and your employer are invested to help build up a pension pot. Generally, the more you put in, the bigger your pot. What you get at retirement is based on how much you’ve contributed and how your investments’ have performed.

- Defined benefit (final salary scheme) – Your employer pays you an income at retirement based on your salary and how long you've worked for them.

State Pension

State Pensions are provided by the Government. Most people can access their state pension in their late 60’s.

To qualify for the state pension, you’ll need to have paid at least 10 years of National Insurance (NI) contributions. To get the full weekly amount, you’ll need to have paid at least 35 years of NI. So how much you’ll receive, depends on how much NI you've paid, while working.

Check out your State Pension forecast and your State Pension age.

How do pensions work?

We can help you understand how your pensions and investments work.

1. Paying into your pension

Workplace pension contributions are automatically taken as a percentage of your salary, before any tax is deducted, each payday.

For personal pensions you can set up regular monthly contributions, transfer in pensions, or make one-off payments.

2. Tax relief

Tax relief is where HMRC tops up your qualifying pension contributions at the basic rate of tax. Higher or additional rate taxpayers could claim extra tax relief through their self-assessment.

Tax treatment depends on individual circumstances and may be subject to change.

3. Investing your pension

Investment options vary between pension types and providers.

Some pensions invest your money in a portfolio of assets, moving from higher to lower risk assets as your near retirement (known as ‘lifestyling’).

Others, such as SIPPs, allow you the control to decide on investments that suit your risk appetite and retirement goals.

4. Taking your money in retirement

When the time feels right to retire, there are several ways to access your pension. You decide how you want to receive your money, with the first 25% normally being tax-free.

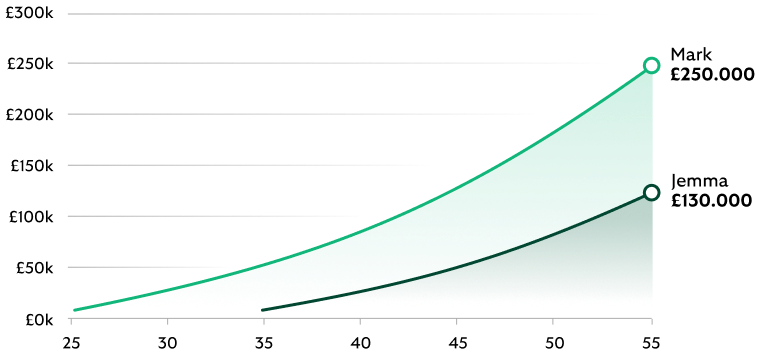

Why have a pension?

Here’s some reasons to pay into a pension:

- Income for your retirement – your State Pension alone might not be enough. Paying into a workplace or personal pension could help offer you a more secure financial future.

- Grow your money – pensions are a long-term investment. They can offer more growth than savings accounts, helping you beat the rate of inflation.

- Tax benefits – pensions are tax efficient. The government pays tax relief on eligible contributions and any growth on investments in your pensions are tax-free.

- Employer contributions – with workplace pensions, usually your employer adds to your pension too, giving you money you wouldn’t have otherwise.

If you want a more short-term way to save or think you may need to access your funds before you’re 55 (rising to 57 in 2028), you may want to consider a savings or investment account.

How much should I pay into my pension?

How much you decide to pay into a pension is based on your personal circumstances. This depends on the lifestyle you want for retirement, and how much you pay into your pension today.

That’s why it’s important to know what you can afford to pay in. This could be smaller, regular payments or larger contributions less often. Remember, you’ll get government tax relief on any payments you make into your pension.

Minimum contributions for workplace pensions are 3% of your annual salary from the employer and 5% from the employee. Some employers may match employee contributions up to a higher percentage.

Our pension calculator can guide you on if your pension is on track to offer you the retirement lifestyle you want.

How and when to take your pension

Our pensions offer you with flexible options at retirement, letting you access your pension when the time is right, and in a way that suits you.

Drawdown (Flexi-access Drawdown)

Gives you a one-off tax-free lump sum of up to 25% and then freedom to choose how and when you take out the rest of your money.

An Uncrystallised Funds Pension Lump Sum (UFPLS)

Allows you to withdraw as much or as little as you like, but 25% of each withdrawal is tax free.

Leave it invested

You can leave your money invested and decide when and how to access your pension later.

An annuity is a way of giving you a one-off tax-free lump sum of up to 25%, and then converting the rest into a guaranteed regular income for life (we don’t offer an annuity, but you can transfer to an annuity provider).

Please see the Retirement options page for more information.

We're all part of Lloyds Banking Group which incorporates many well-known companies including Lloyds, Scottish Widows, Halifax Share Dealing Ltd and Embark Investment Services Ltd. Our retirement partner for this SIPP is Scottish Widows, who have more than 200 years' experience in pensions and retirement.

Let’s look at the details

-

These limits are the total amount of tax-free lumps sums you can take from your pensions.

Annual Allowance

This is the amount you can contribute across all your pensions each year tax free. This tax year it’s £60,000 (or 100% of your earnings, if you earn less than this).

Lump sum allowance:

HMRC applies a limit to the lump sum(s) you can take tax-free. This is called the Lump Sum Allowance (LSA). This tax year the limit is £268,275. Your tax-free Pension Commencement Lump Sum (PCLS) is limited to 25% of your pension value, up to a maximum of the LSA (unless you have existing pension protections in place).

Money Purchase Annual Allowance:

The Money Purchase Annual Allowance (MPAA) limit applies once you start taking income from your SIPP – this could be a withdrawal from your flexi-access drawdown or taking a taxable lump sum (UFPLS). The MPAA limits impacts the amount you can pay into your SIPP in the future without incurring a tax charge. This limit is currently £10,000 each tax year (although the Government may change this in future).

Lump Sum Death Benefit Allowance (LSDBA)

This is a limit applies to level of tax-free death benefits. This tax year the limit is £1,073,100. The LSDBA will be reduced by Relevant Benefit Crystallisation Events (RBCEs) – effectively, withdrawals already taken from your pension before your death.

Death benefits paid as a flexible income through a beneficiary drawdown are not subject to the LSDBA.

You may be able to carry forward up to three previous tax years’ worth of unused allowances.

-

One of the benefits of investing into a pension is tax relief. If the basic rate of tax is 20%, for every £80 you pay in, the government usually adds an extra £20.

If you’ve told us you’re eligible, we’ll automatically add basic rate tax relief to any regular or one-off contributions you make into your Ready-Made Pension or SIPP. If you’re a higher rate taxpayer, you can claim additional tax relief through your self-assessment tax return.

You don’t receive tax relief on any transfers into your pension. Employer contributions are paid gross of tax (limited company directors only).

Tax treatment depends on your individual circumstances and tax rules may change in the future.

-

We can’t give you financial advice.

If you want this, you could speak to an Independent Financial Adviser. Unbiased and Vouchedfor will help you find a local adviser based on your requirements. There will normally be a charge for this service.

You also get free help and guidance through Pension Wise. If you’re over 50, you’ll also benefit from a free 60-minute appointment.

Alternatively, Lloyds Wealth could also help. Personalised advice is available across a range of products and services. It all starts with a free, no obligation chat, then a financial plan that’s tailored to you. To be eligible, you’ll have at least £100,000 in sole or joint savings, investments or personal pensions, or sole income of at least £100,000. Fees and charges may apply.

-

If you’ve decided that you’d like to change your regular income, please complete this short form and we’ll be in touch.

You can update the following at any time:

- Amount of your pension income.

- Payment date

- Payment frequency

- Bank details.

Please be aware any of the above changes will usually take up to 10 working days to complete.

If you're increasing your income payments from your Self-Invested Personal Pension (SIPP), please be aware of the following:

Sustainability of funds: Ensure you have sufficient funds to support the increased withdrawals over the remaining term of your retirement. Drawing too much too soon could deplete your pension earlier than expected.

Tax Implications: Increasing your income may push you into a higher tax bracket. This could result in a larger portion of your income being taxed at a higher rate. We recommend seeking tax advice to understand the full impact.

Investment suitability: Review your investment choices to confirm they remain appropriate for your needs. Your investment strategy should align with your income requirements and retirement needs.

If you need any help and guidance, you can get this free through Pension Wise. If you need any financial advice, You can visit Unbiased or Vouchedfor to find a financial adviser near you. They will charge you for this service.

You may also like

Pensions calculator

Estimate your retirement income. Adjust contributions or retirement age to see changes.

Top tips

Our tips could help make your pensions work harder.

Educational videos

Our experts are here to answer the most common pension questions.

Important legal information