Life insurance

Life is a work in progress. Protect the ones you love with life insurance from Scottish Widows.

Get your quote now

Our insurance services are rated excellent on Trustpilot.

Enjoy 12 months of Disney+ on us!

Get 12 months of Disney+ (Standard With Ads) when you purchase a new protection policy directly with us.

With blockbuster movies, new originals, and much-loved shows, there’s something for everyone to enjoy.

Stream endless entertainment and relax, knowing we've got you covered.

Your subscription starts after you make your first payment.

We can amend or withdraw this offer at any time. Terms and conditions apply.

Understanding our life insurance

Types of life insurance

Life insurance calculator

Get covered

Scottish Widows provide our life insurance policies and are part of Lloyds Banking Group.

The cost of life insurance depends on things like your age, health and lifestyle. As well as the amount of cover and length of time you need it for. Premiums start from £5 a month* and you can get a quote online to get a better idea of how much your cover could cost you.

*6% of Lloyds Bank customers paid £5 a month for Plan and Protect life insurance bought online between 01 January 2024 to 31 December 2024. Price is based on single level life insurance, excluding critical illness cover, and is subject to underwriting criteria that depends on personal circumstances. Prices are subject to change.

Let’s look at the details

-

Apply online

You must be aged 18 to 59 and looking for up to £500,000 level term cover on a single life basis.

To apply over the phone

You must be aged 18 to 79 for life cover and 18 to 64 for critical illness cover. You can apply for up to £18 million in life insurance and up to £3 million in critical illness cover. This can be on a level, increasing or decreasing basis, single or joint life cover.

Lloyds protection experts can help you decide what you'll need and assist you with your quote. You'll receive details on Scottish Widows life insurance policies.

-

You can still get life insurance with existing medical conditions. However, acceptance depends on the health issues you have and it may cost more. Insurers are likely to view people with pre-existing conditions as higher risk when providing cover.

Life insurance companies review all policies on a case-by-case basis, taking into account your medical history. So, it can depend on your individual circumstances. Some conditions may have a bigger impact than others on how much you’ll have to pay.

If you have a serious medical condition, your options and the costs may be more limiting.

-

Changing jobs

Changes to your income could impact the level of cover you and your family need if the worst was to happen.

Growing your family

When your family grows, the need to protect them can change. This could be a good time to make sure they are in the best possible position if anything were to happen to you.

Buying your home

When buying your home, you may want to protect it. This could allow your loved ones to pay off the mortgage and stay in their home.

Getting married

This can be a good time to think about how cover could help to protect your partner in case of the unexpected.

Divorce/separation

Getting a divorce or separating is a significant life change and it can impact your financial situation and responsibilities.

Becoming a carer

There might be others who rely on you or your income. Your cover could protect them too.

-

Download or view our policy guides:

You may also like

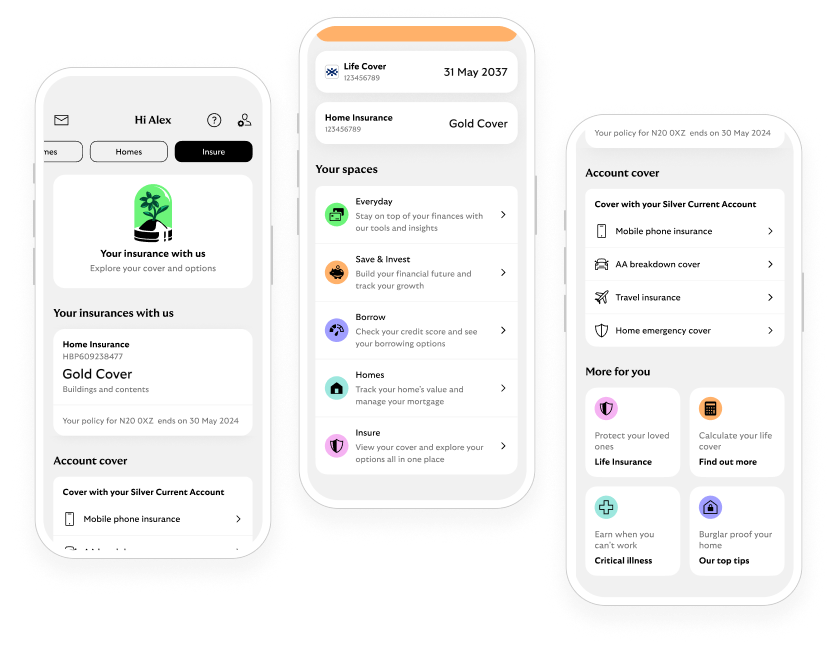

Life insurance in your pocket

Check your cover or manage your policy, anytime, in our app.