Mortgage Statements

Your annual statement explained

Let us help you understand your annual mortgage statement. This guide is intended for use by customers with an account number beginning with 40 or 80 who receive annual statements.

Each section on this page corresponds to part of your Lloyds Bank mortgage statement. Use the labelled diagrams within each section to help you find out about what’s in your statement and what it means.

- Summary of your mortgage account.

- Account transactions.

- Other items in your statement.

- Sub account transactions.

You can also use the frequently asked questions which lists common mortgage statement queries.

If you have any further questions please call us.

-

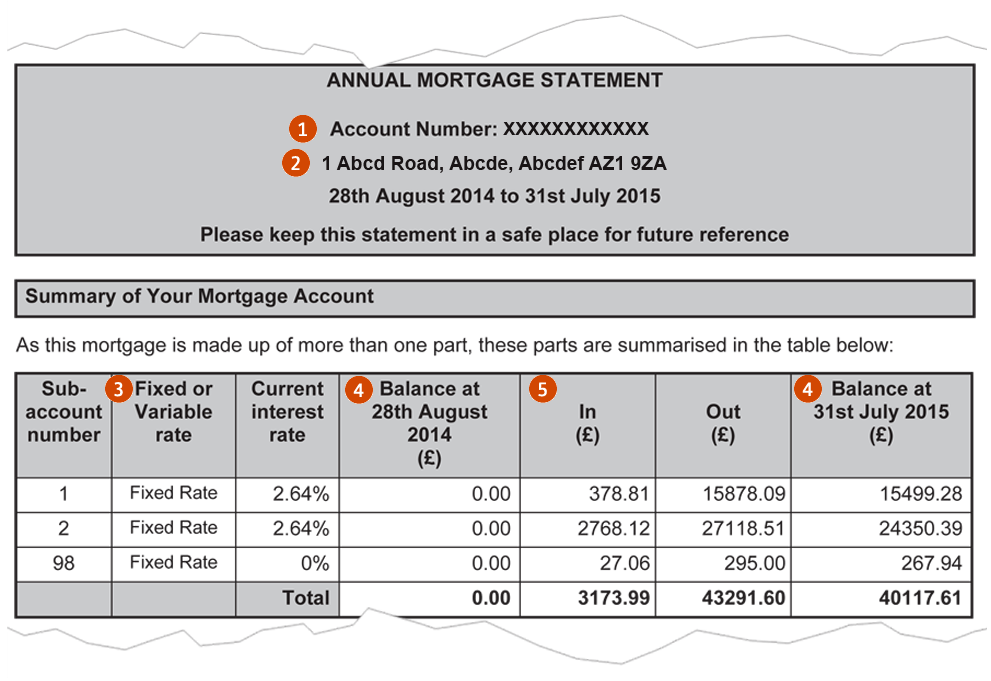

1. Account Number - This is your mortgage reference number; please use this when you are contacting us about your mortgage.

2. Address - The address of the mortgaged property.

3. This confirms the type of products you are on:

- Fixed rate mortgage - the interest rate remains the same for a fixed period.

- Variable rate mortgage - the interest rate may vary depending on the Bank of England base rate or rates set by Lloyds Bank.

You may have a combination of both types, so both may apply.

- Current interest rate – this is the current interest rate applied to each sub account.

4. Balance at the start and end of the statement period

Column 4 shows the sub-account and total balance of your mortgage at the start of the statement period. Column 7 shows the sub-account and total balance of your mortgage at the end of the statement period.

5. In - Shows the total credits made to each sub-account throughout the statement period and the total amount paid to your mortgage.

Out - Shows the total debits to each sub-account. This could include interest and fees and shows the total amount added to the mortgage.

Find out more with our frequently asked questions

You can check your mortgage balance, monthly payment and interest rate with Internet Banking. Logon to Internet Banking

-

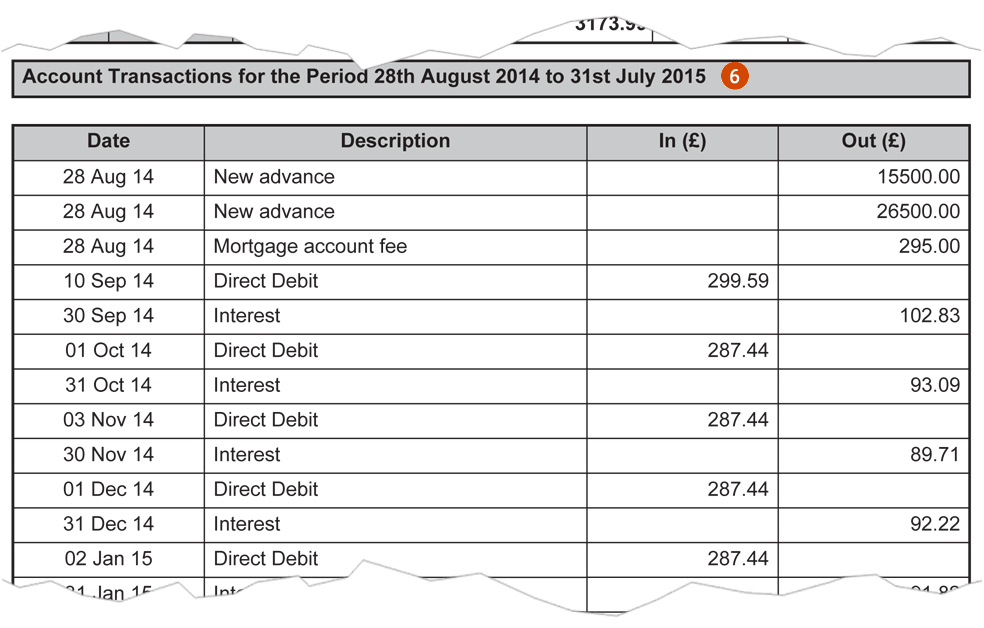

6. Account Transactions – Shows the transaction type for example Direct Debit, Interest, Product Fee, Mortgage Account Fee and the credits and debits during the statement period.

Find out more with our frequently asked questions

You can check your mortgage balance, monthly payment and interest rate with Internet Banking. Logon to Internet Banking

-

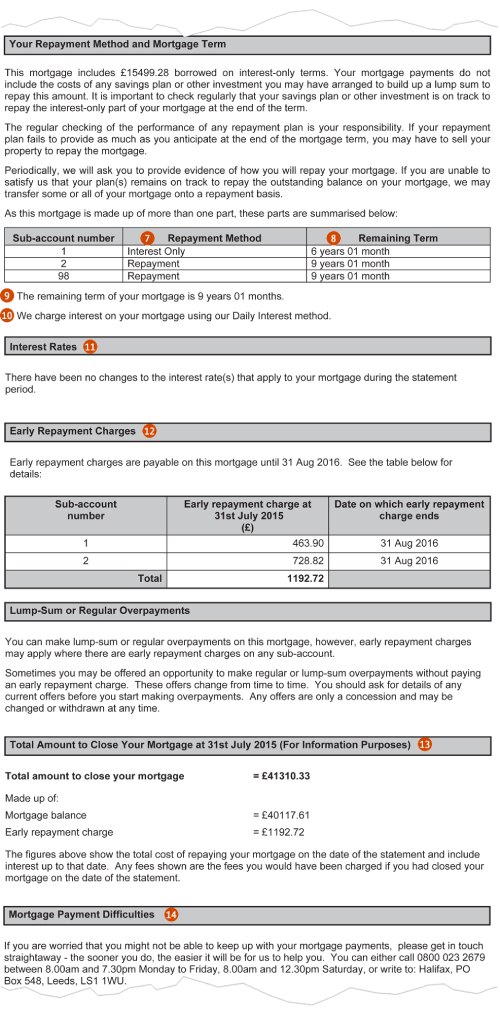

7. This is the repayment method for each sub account. There are three different ways of repaying your mortgage. These are repayment, interest-only and a combination of repayment and interest-only.

8. This is the remaining term for each of the sub accounts.

9. This is the term of the longest sub-account.

10. This confirms whether the interest on your mortgage is calculated on a daily or annual basis. If you are paying interest on an annual basis, you may be able to save money if you switch to daily interest.

11. Interest Rates – shows rates charged during the statement period.

12. Early Repayment Charges - the charges shown are those that you would pay if you repaid the mortgage on the date of the statement. Also included is the date when early repayment charges no longer apply. If there are no early repayment charges applicable to your mortgage, this section will not appear on your statement.

13. Total amount to close your mortgage - If you had chosen to repay your mortgage on the date shown, this is the total amount that would have been repayable including interest and fees (see the break down below). These figures will change day to day.

14. Mortgage payment difficulties - if you are currently finding it difficult to pay your mortgage and believe you may be facing into financial difficulties please don’t ignore the problem, there are ways we can help.

Find out more with our frequently asked questions

You can check your mortgage balance, monthly payment and interest rate with Internet Banking. Logon to Internet Banking

-

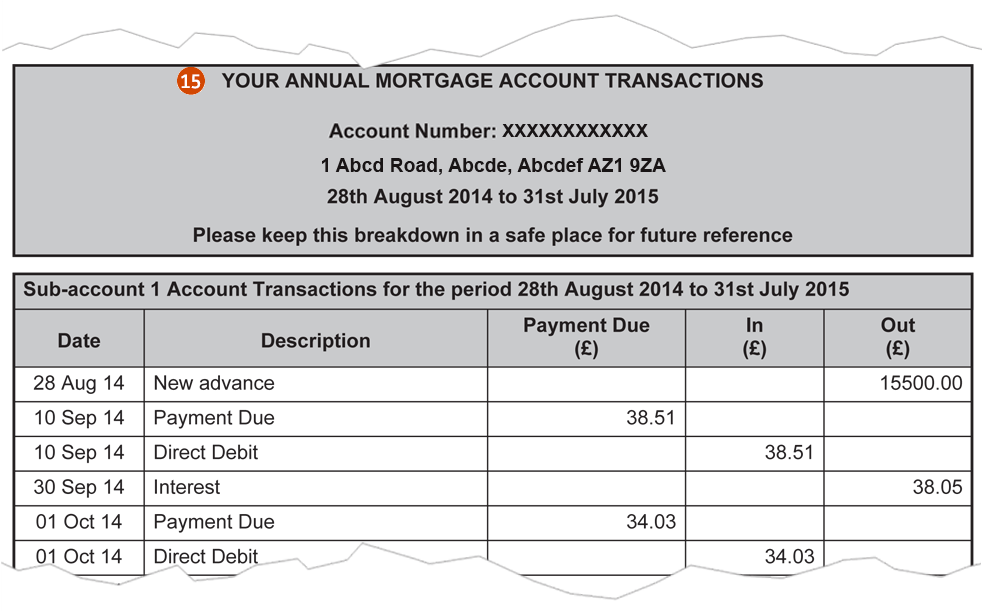

15. This section shows all the account transactions for this sub account. Your annual mortgage statement will include one transaction breakdown per sub account.

For a summary of your full mortgage balance, please see the first page.

Find out more with our frequently asked questions

You can check your mortgage balance, monthly payment and interest rate with Internet Banking. Logon to Internet Banking

-

When should I receive my annual mortgage statement?

Your statement is sent to you on a yearly basis within four weeks of the anniversary of your mortgage account start date.

What is a sub-account?

Your mortgage may be split into multiple parts called sub payments. Each sub-account may have a different repayment method, interest rate and term.

The total monthly payment is made up of all the sub-account payments. When the total monthly payment comes in, we split it to give each sub account the amount it needs. If you overpay or underpay, each sub account is given its share of the total amount received.

What are sub-accounts 98 and 99?

Sub-account 99 holds fees. Some customers may also have a sub-account 98 if they have a mortgage account fee.

How much can I overpay by without being charged early repayment charges?

If you have a mortgage without early repayment charges you can overpay unlimited sums on your mortgage each year. Your mortgage statement should tell you if you have any early repayment charges.

For any sub-account where an early repayment charge applies, currently as a concession, in each calendar year you can make regular or lump-sum overpayments of up to 10% of the amount owed at 1st January without having to pay an early repayment charge.

For example, on a mortgage balance of £200,000 you can overpay by up to £20,000 as either a lump sum or regular monthly overpayments in one calendar year.

Why have you charged me an early repayment charge?

If your mortgage agreement is subject to an early repayment charge, we will apply the early repayment charge in the following circumstances:

- You have made one or more overpayments totalling over 10% of your mortgage balance in one calendar year.

- You have repaid your mortgage in full before any early repayment charges which were present on the account have expired.

Why am I charged more interest in some months than others?

Where your interest is calculated on a daily basis, this means that the number of days in each individual month determine the number of days worth of interest charged.

For example, January has 31 days and February has 28 days (or 29 in a leap year), this means the interest for each month will be different.

Where your mortgage is on a repayment basis each monthly payment you make reduces the overall mortgage balance we use to calculate interest and as a result reduces the amount of interest charged.

Why is my mortgage balance increasing?

There are a number of reasons your mortgage balance may increase including:

- Your monthly payments have not been made.

- Your monthly payments are only partially made.

- Additional fees may have been added to the mortgage (this could include Product, Additional Borrowing, and Arrears Fees).

- Unpaid insurance premiums that are linked to the mortgage.

- If you have had a payment holiday.

- You have changed the due date for your payments.

If your mortgage balance has decreased, this may be due to previous overpayments made.

Go paper free

Get your annual statements in the app or online banking.

You may also like