Mortgage basics guide

Our mortgage basics guide covers what you will need to think about when looking for a home and applying for a mortgage.

-

Initial mortgage costs

Whether you are buying a new property, moving your current mortgage to us from another lender, or borrowing more money, it is important to know how much it is all going to cost.

We usually expect you to be able to provide a deposit but there will be other costs too, especially if you are moving home. You need to think about whether you can afford all these costs.

Deposit

We will only lend you a percentage of what the property is worth, so you will need to put down some of your own money towards the cost. We call this a deposit. Your deposit should be at least 5% of the property’s value (apart from our Lend a Hand mortgage). If you can put down more than 5%, you can often get a lower initial interest rate.

Other costs

There are other costs in buying a property and taking out a mortgage. Here are some typical ones that apply to most buyers.

Other costs in buying a property and taking out a mortgage Cost

Summary

Cost

Valuation of property

Summary

Your mortgage adviser will discuss valuation schemes and fees with you when you make your full application. The fee depends on the property value and the type of valuation you choose.

Cost

Conveyancing fees

Summary

Charged by a conveyancer for doing the basic work connected with buying your property. Fees can vary and are often based on the purchase price plus other costs.

Our conveyancing service allows you to compare quotes from up to 200 conveyancers.

Cost

Government Land Tax

Summary

This is a government tax charged on land and property transactions in the UK. The tax is charged at different rates depending on property and values of transaction. Government Land Tax is known differently depending on which country you are purchasing a property, i.e. in England it is known as Stamp Duty.

For more information, visit our stamp duty page.

This tax is an expensive extra cost that you should take into account when thinking about buying property.

Cost

Land Registry fees

Summary

The Land Registry will charge for any searches of the property register the conveyancer asks for. It also charges for registering you as the owner and us as the lender. You must pay both these costs.

Cost

Local authority search fees

Summary

The local authority will charge for answering your conveyancer’s questions about the property you want to buy, such as whether the local authority maintains the roads adjoining the property or whether you will be responsible for this.

Cost

Other relevant property searches e.g. mining or environmental searches

Summary

Sometimes your conveyancer will have to carry out other searches because of where your property is. These may be environmental searches to check if certain industrial processes are carried out in the area or if the property is built on land that may have been contaminated because of the way it has been used in the past. Mining searches ask for records of any mining work that may affect the property. The organisations that answer these questions will charge for this, and you will have to pay these costs.

There are often unexpected costs in buying a property, so it is a good idea to have a reserve fund to cover them.

There could be other charges and standard costs which you may have to pay during the course of setting up your mortgage.

-

Property types

We will consider lending you money to buy different types of old and new property, purpose-built flats or conversions, or a property you are buying outright or under an approved shared ownership or shared equity scheme.

We will also consider an application to buy a property that you want to rent out to someone else. We may ask you to provide a bigger deposit on some types of property than others.

Any loan we make will be subject to a satisfactory property valuation by a surveyor of our choice.

Freehold

If the property is freehold, then you will own the property and the land it is built on. We do not lend on freehold flats in England and Wales or Northern Ireland.

Leasehold

If the property is leasehold, then you will own a temporary right to occupy the property and the land it is built on. The property and the land are owned by someone else and they lease them to you for a number of years. Leases can last for decades or centuries. There is usually an annual charge for the lease, called a ground rent and sometimes there may also be service charges.

We will only lend on leasehold properties with at least 70 years left on the lease when you apply. Before you buy, your conveyancer will check the lease terms to make sure they are acceptable.

In Scotland (except in rare cases where there is a form of long lease known as a 'tack') all properties are owned outright by the 'registered proprietor'.

New build or converted properties

A new property or a property that has been built or converted within the last ten years should be part of a Building Standards indemnity scheme. This gives a ten-year warranty against material defects. There are a number of acceptable schemes, but the main one is run by the National House-Building Council (NHBC).

We will consider lending on properties that are not part of one of these schemes if it comprises of a development of no more than 15 properties and meets our current monitoring requirements.

Help to Buy

Lloyds Bank supports a range of government backed initiatives to help people buy a home. For more information, you can speak to one of our mortgage advisers. Or visit the government website.

Shared equity

This can take various forms. Usually you own 100% of the property but pay a reduced amount to the builder, for example 75% of the property value. You own 100% of the property so there is no rent to pay. The builder holds a 25% stake in the property and registers this interest in your property at the Land Registry.

At a later date, when you can afford to, you can buy the remaining 25% from the builder at a cost of 25% of the property's value at that time. If you decide to sell the property, you must give the builder 25% of the sale proceeds.

Shared ownership

Shared ownership schemes are usually offered by registered social landlords or local authorities. With this type of purchase you buy a share of a property, say half, and pay a reduced rent for the rest to the registered social landlord or the local authority.

The share you first buy may be as little as 25%, but if you wish you can buy more shares later until you own the property outright.

Right to Buy

If you rent your home from your local authority or a registered social landlord, you may have the Right to Buy your home under certain conditions set out by your landlord. You may be able to buy your home at a discount to its market valuation. The discount is usually based on the property value and how long you have been a tenant.

Buy to let

A buy to let mortgage is a loan you can take out to buy an investment property that you or your family won’t live in and that you intend to rent out to tenants.

Taking out a mortgage is one of the many risks of investing in buy to let properties. So before you enter the market you should be an experienced house buyer and have fully researched investment properties.

These mortgages aren't available to first time buyers or applicants under the age of 21. At least one person named on the loan must currently own a property in the UK.

Whether you are starting or expanding your property portfolio, we are here to help you get the right mortgage deal with our range of buy-to-let mortgage products.

-

Valuation schemes

A mortgage valuation helps us make a decision on your application. With exception to remortgages and additional borrowing, when you apply for a mortgage, we'll ask you to choose from two levels of inspection and report. Unless we tell you otherwise you will have to pay the cost of this. Once the valuation has taken place the fee for this is non-refundable. In Scotland the seller of a property has to get a Home Report, which contains a property valuation. We may accept the valuation if the surveyor is RICS accredited.

To help with your decision to buy it is important that you understand the property’s condition and any issues that may affect its value. If you want a more detailed report than the level 1 or level 2 valuation we offer, you may wish to consider a full building survey. You will need to make your own arrangements to get one. To do this you can use a RICS accredited surveyor, they can be found at www.ricsfirms.com.

A building survey will give you a customised report, based on the agreement between you and the surveyor. We will still need to complete a mortgage valuation, which you will need to pay for. We need this to help us make a decision on whether we will lend you the money to buy the property.

Please see the table below for details about the different types of valuation you can choose.

Types of valuation Mortgage Valuation

(Level 1)HomePlus Survey

(Level 2)Building Survey

What it is

Mortgage Valuation(Level 1)

A basic property valuation for the Bank that is purely to help us make a decision on whether we will lend you the money to buy the property.

This may not be a physical inspection of the property or produce a report. It is limited and property defects may not be identified.

It is used for lending purposes only, so if you require a more detailed inspection, you may wish to consider a level 2 valuation or arranging for your own building survey.

HomePlus Survey(Level 2)

A HomePlus Survey will give a more detailed analysis of the property’s condition and defects and a comprehensive digital report for you.

A valuation is provided to us to help us make a decision on whether we will lend you the money to buy the property.

Building Survey

This is the most detailed type of survey available and you can tailor it to meet your needs.

We cannot arrange this type of survey for you and can’t recommend a surveyor, but can provide details to help you find an RICS accredited surveyor.

We will still need to arrange a separate Mortgage Valuation for lending purposes and you will need to pay the fee for this if applicable.

How it’s done

Mortgage Valuation(Level 1)

We will decide if we want a surveyor to visit and assess the property or we may use a combination of historical and market data to compare your property to others in the local area.

HomePlus Survey(Level 2)

A surveyor will visit to assess the inside and outside of the property.

Before this happens, the surveyor will send you the terms of their agreement for you to accept.

Building Survey

You will need to arrange this type of survey yourself.

Usually, once instructed, you will discuss matters with your surveyor to agree what will be covered by the report and any concerns you may have about the property. An internal and/or external inspection of the property will follow, based on your requirements.

What you get

Mortgage Valuation(Level 1)

If a surveyor has visited the property you will get a copy of the report. It will give very limited information about the property.

If a surveyor has not visited the property, there will be no report to provide. Instead we will tell you if our assessment of the value means we will not lend you the loan amount requested.

HomePlus Survey(Level 2)

The survey gives you guidance on the essential things you may need to know about the property, such as defects and problems that are serious or that may significantly affect the value.

Building Survey

A customised report based on the agreement between you and the surveyor.

What it means for you

Mortgage Valuation(Level 1)

Defects that could affect your decision to buy may not be identified, and it should not be relied on for your buying decision.

HomePlus Survey(Level 2)

It does not give a full structural assessment.

Whilst it may give details of issues with the property, it may not go into the level of detail you require.

You will not get a copy of the basic valuation report provided to us.

Building Survey

As this is a customised report you get to choose what is included within the report.

We will still need to arrange a separate Mortgage Valuation for lending purposes and you will need to pay the fee for this if applicable.

-

Repayment methods

There are three different ways of repaying your loan. These are repayment, interest-only, and a combination of repayment and interest-only.

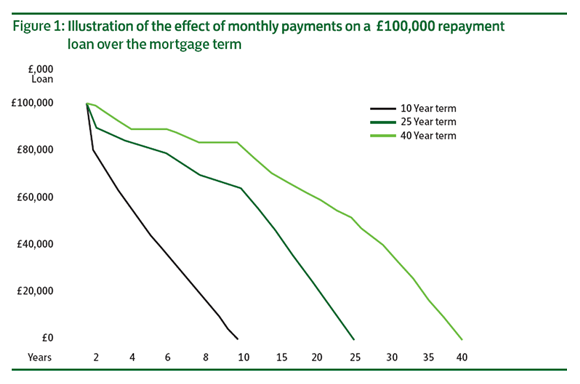

Repayment

Every month, your payments go towards reducing the amount you owe as well as paying off the interest (see Figure 1). This means that each month you are paying off a small part of your loan. Your annual statement will show your loan getting smaller. However, in the early years your monthly payments will mainly go towards paying off the interest, so the amount you owe won’t go down much at the start.

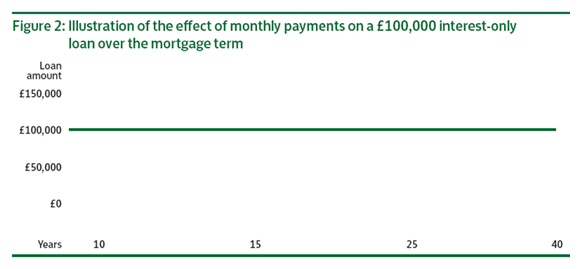

Interest-only

Your monthly payment pays only the interest charges on your loan - you don't pay off any of the loan amount (see Figure 2). This means your monthly payments will be less than if you had a repayment mortgage. However, the total cost of an interest-only mortgage will be higher because you will be paying interest on the full loan amount throughout the mortgage term.

With an interest-only mortgage, you will need to know from the start how you are going to find a lump sum to repay the loan at the end of the mortgage term. When you apply, we'll ask you to show us that you have a repayment plan(s) in place, to pay off everything that you owe at the end of the mortgage term.

From time to time, we will ask you to show us that your repayment plan(s) remains on track to pay off everything you owe by the end of your mortgage term, and you must show us if we ask you. It’s important that you keep checking that your arrangements are still on track.

If we think your plan may not be enough to repay everything you owe at the end of the term, we may contact you to discuss your plan and what can be done to put it right. For example you could consider transferring part, or all, of your loan onto a repayment mortgage.

It’s your responsibility to make sure you have enough money to repay everything you owe at the end of your mortgage term. If your plan(s) does not give you enough money to repay everything you owe at the end of the term, you may have to sell your property.

Interest-only mortgages are only available when the amount of loan is less than 75% of our latest valuation of the property.

Acceptable repayment plans

The table below sets out the repayment plans we currently accept which may change in future.

Acceptable repayment plans Acceptable plan types

Information you must give us

Our assessment of acceptable values

Acceptable plan types

Endowment policies (UK)

Information you must give us

Copy of latest projection statement dated within the last 12 months.

Our assessment of acceptable values

Endowment companies will present three growth rates.

We allow up to 100% of the projected amount using the middle figure.Acceptable plan types

Stocks and shares (UK)

Information you must give us

Copy of share certificates, nominee account statement or confirmation from a recognised broker containing evidence of share holdings and their valuation.

Our assessment of acceptable values

We will accept up to 80% of the latest valuation of the stocks and shares, ISA, OEIC or investment bond (if the latest valuation is greater than £50,000).

Acceptable plan types

Stocks and shares ISA (UK)

Information you must give us

Copy of latest statement dated within the last 12 months.

Our assessment of acceptable values

As above.

Acceptable plan types

Unit trusts, open-ended investment companies (OEICs) (UK)

Information you must give us

Copy of latest statement dated within the last 12 months.

Our assessment of acceptable values

As above.

Acceptable plan types

Investment bonds (UK)

Information you must give us

Copy of latest statement dated within the last 12 months.

Our assessment of acceptable values

As above.

Acceptable plan types

Pension (UK)

Information you must give us

Copy of latest projection statement dated within the last 12 months.

Our assessment of acceptable values

For the purpose of backing an interest-only mortgage, we can use a maximum of 15% of the latest projected value if this projection is greater than £400,000.

For Final Salary schemes: we can use a maximum of 60% of the tax free lump-sum amount, provided the projection shows a minimum lump-sum available of £100,000.

Acceptable plan types

Sale of second home (UK)

Information you must give us

Property details, confirmation of ownership, evidence of the amount of any mortgage debt.

Our assessment of acceptable values

We will check the ownership of the property and assess its value. We will deduct any amount you owe that’s secured against the property and allow you to use up to 80% of the amount left over (if this is over £50,000).

Combination of repayment and interest-only mortgage

It is possible to split a mortgage between repayment and interest-only. This means that at the end of the mortgage term you will still have an amount of the mortgage to pay off, which you will need to do using a lump sum.

So, as with an interest-only mortgage, you will need to make sure you have a plan to repay this amount at the end of the term.

-

Mortgage products

We have different types of mortgage products with different types of interest rates. These change from time to time and we will give you details of the current range when you apply.

Your mortgage adviser will discuss your needs and circumstances with you before recommending the most suitable mortgage for you. They will give you a Mortgage Illustration that sets out the loan’s total cost and gives essential information about the product(s) you're interested in.

The Mortgage Illustration includes an Annual Percentage Rate of Charge, usually called an ‘APRC’. This is an annual interest rate which takes account of fees and charges to reflect the total cost of your mortgage. Your Mortgage Illustration will detail the fees which are included in this calculation. An APRC is calculated using a standard method so it provides an effective way for you to compare quotes from different lenders.

Type of product

How it works

Early repayment charges

What it means for you

Is it right for you?

Type of product

Fixed rate

How it works

Your interest rate is set at a certain level for an agreed period (the product rate period).

At the end of that period, we switch you to another rate, usually one of our Lloyds Bank lender variable rates.

Early repayment charges

Early repayment charges usually apply during the product rate period.

What it means for you

Your interest rate will stay the same during the product rate period, even if the Bank of England base rate or our Lloyds lender variable rates change.

A fixed rate gives you the security of knowing your interest rate won’t change.

Is it right for you?

Ask yourself if being certain that your interest rates won't rise is more important than the possibility of paying a lower interest rate.

With a fixed rate, you won't benefit from any falls in the interest rate during the product rate period.

Type of product

Tracker rate

How it works

This is a variable rate that is above, below or the same as the Bank of England base rate or some other rate it tracks for an agreed period.

At the end of that period, we will switch you to another rate, usually one of our Lloyds Bank lender variable rates.

Early repayment charges

Early repayment charges usually apply during the product rate period.

What it means for you

It can pay to have a tracker if you can afford to pay more when interest rates rise so that you can benefit when they fall.

Is it right for you?

Ask yourself if you're confident that you'll be able to make your monthly payments if interest rates rise.

Type of product

Lloyds Bank lender variable rates

How it works

A variable rate we set. We can change our lender variable rates at any time. We will only increase them because of a change to our cost of lending, a change to laws and regulations or a change to our technology or systems that cause our costs to change. You can read more about this in the Mortgage Conditions.

We have more than one Lloyds Bank lender variable rate, and we may change one rate at a different time or by a different amount to another of our lender variable rates. Your Mortgage Illustration and offer letter say which rate(s) applies to you.

These rates aren't available as a stand-alone product. They are usually a rate we switch you to at the end of your product rate period.

Early repayment charges

Early repayment charges don't usually apply, but check your Mortgage Illustration or offer letter to be sure.

What it means for you

If you stay on a Lloyds Bank lender variable rate you’ll need to consider if you can afford the monthly payments when interest rates rise so that you can benefit when they fall.

Is it right for you?

Ask yourself if you're confident that you'll be able to make your monthly payments if interest rates rise.

You may be able to swap onto a different rate by doing a Product Transfer.

-

Legal work

Understanding the role of the conveyancer and the Legal work will ensure there are fewer surprises along the way.

You will need a conveyancer to do the legal work for us, and you will have to pay their costs.

You can do your own legal work, but we advise you to employ a conveyancer to look after your interests and to explain and deal with complex paperwork. Buying a property is complicated, especially if it involves shared ownership or shared equity.

You can use different conveyancers to deal with our work and yours, but it is normally easier to use the same conveyancer to deal with both.

You must appoint a solicitor or licensed conveyancer (in Scotland they must have a practising certificate issued by the Law Society of Scotland) and the conveyancer doing our work must be a member of our approved panel.

The role of a conveyancer

The conveyancer will:

- Give you legal advice on all aspects of buying a property.

- Unless the property is in Scotland, get a purchase contract from the seller’s conveyancer with details of the property and its ownership.

- In Scotland, exchange missives with the seller's solicitors and carry out a title check on the property.

- Sort out all pre-contract enquiries (in Scotland, check that all the conditions of the missives have been met); get copies of existing guarantees and so on.

- Get the seller’s fixtures and fittings list to see what they will be leaving in the property and check with you that this list includes all that you agreed would be included.

- Check your offer letter when it arrives and explain any parts of it and the mortgage conditions that you don’t understand.

- Except in Scotland, arrange for you to sign a copy of the contract, agree a completion date and exchange contracts with the seller’s conveyancer.

- In Scotland, conclude missives with the seller's solicitor including an agreed date of settlement.

- Ask you to pay your deposit and ask us to send them your loan money.

- On completion day, pay the required amount to the seller’s conveyancer and arrange for you to collect the keys.

- Register your ownership of the property and the mortgage at the Land Registry/Registers of Scotland and pay any Government Land Tax.

Selected remortgages may come with our Remortgages Service where we'll pay our own legal fees and won't charge you for the property assessment.

Legal contracts

When you agree to buy or sell a property, you enter into a contract with other people you have agreed to buy from or sell to.

Once the contract terms have been agreed, each party to it signs a copy and agrees a completion date, and the contracts are exchanged – in Scotland this is known as the conclusion of missives.

Your conveyancer will take care of this and check that all the legal conditions are met.

Before exchange of contracts

At any time before exchange of contracts the seller or the buyer can change their mind, normally without having to make a payment to the other:

- The seller can accept a higher offer from somebody else – called gazumping.

- The buyer can withdraw the original offer and make a lower one – called gazundering.

Before exchange of contracts the seller's conveyancer will usually:

- Obtain details of the seller's legal title to the property.

- Ask the seller to fill in a Property Information Form and a Fixtures and Fittings and Contents form. These forms collect information about the property and what is included in the purchase price.

- Agree the content of the contract of sale with your conveyancer.

- Answer any questions raised by your conveyancer.

- Ask the seller to sign one of the contracts.

Before exchange of contracts, your conveyancer will usually:

- Read the documents sent by the seller's conveyancer.

- Make a local search and a drainage search. They may also do other searches depending on where the property is, for example environmental or mining searches – in Scotland this is done by the seller's conveyancer. Learn more about property searches

- Ask the seller's conveyancer any necessary questions.

- Receive a copy of your offer letter from us and any formal instructions about acting for us.

- Report to you and ask you to sign a copy of the contract.

At exchange of contracts

On exchange of contracts you have to pay a deposit. Normally this is 10% of the purchase price.

If a buyer or seller backs out of the sale after exchanging contracts, they are breaking a legally binding agreement. They will almost always have to pay the other person compensation.

You should contact your chosen buildings insurance provider and ask them to start cover as soon as you have exchanged contracts.

After exchange of contracts

Between exchange of contracts and the completion date, your conveyancer will usually do the following:

- Make searches at the Land Registry to make sure nothing new has come to light since the seller’s conveyancer obtained the original copy of the property registry entries – in Scotland, the seller's conveyancer will do this.

- Contact your current lender (if any) and ask how much is still owing on your existing mortgage.

- Ask you to sign a transfer document, a land transaction return, the mortgage deed (Standard Security in Scotland) and any other documents we need you to sign.

- Ask us to send the loan money ready for the conveyancer to send to the seller's conveyancer on the day of completion.

- Ask you for any remaining money needed to buy the property.

When the mortgage starts

On the day of completion, your conveyancer will pay the seller's conveyancer the balance of the purchase price. Ownership of the property is transferred to you and you become entitled to have the keys and move in.

The seller's conveyancer will pay off the seller's mortgage and send your conveyancer the transfer document and any other relevant documents, for example property guarantees.

Your conveyancer will then register your ownership and the mortgage at the Land Registry/Registers of Scotland and pay any Government Land Tax owing to HM Revenue and Customs.

If you have an existing loan that must be repaid, your conveyancer will send the money to your current lender and that loan will end.

Ownership of the property

When two people buy a property together they are normally registered at the Land Registry as co-owners. There are two main ways of co-owning property, and the legal terms for these are ‘joint tenants’ and ‘tenants in common’.

With joint tenants, the law regards the co-owners as owning the whole of the property between them. When one of them dies, the whole of the property passes to the other. Usually, the survivor only needs to provide a death certificate to prove their entitlement to full ownership. Joint tenancy is a much used form of ownership between married and civil partners.

However, family matters can be complex and you may not want complete ownership of the property to automatically pass to the other co-owner. If so, you may want to consider asking your conveyancer to register you as tenants in common.

If you own your property as tenants in common, each of you owns only a share in the home. This could be 50/50, but if one of you puts down a bigger proportion of the deposit, you may want to take unequal shares, for example 60/40. If you die, your share will pass into your estate and be dealt with in line with the terms of your will (or the rules of intestacy, if you don’t leave a will).

This way of holding the property may be useful if you are unmarried or have children from a previous relationship. It can also be used as part of estate planning (to try to pay less inheritance tax).

You should ask your conveyancer to explain more about the ways two or more people can own a property.

Occupation of the property

Except in Scotland, anyone over 17 years old who is not your son or daughter but who will be living at the property to be mortgaged will have to sign a consent to the mortgage form.

By signing this they agree not to claim tenancy rights if we take possession of your property because you do not keep up your monthly payments.

Agreement in Principle

An Agreement in Principle will help you search for a property in your price range. It may also help you negotiate a better price with the seller because they know you can get a loan.

An Agreement in Principle, also known as a 'Decision in Principle' or 'Mortgage Promise', is useful if you haven’t found a property you want to buy but would like to know how much you could borrow.

All we need is a few personal details about you and anyone else who will be named on the mortgage. Then we will contact a credit reference agency for a soft credit check and give you a credit score. If you reach our pass mark, we will give you a certificate so that you can show the seller you can get a loan.

Soft credit checks do not affect your credit rating or ability to borrow from lenders in the future. Soft credit checks are not seen by other lenders and can only be seen by you on your credit report.

While we aim to lend you the amount agreed in principle, sometimes we may not be able to lend you as much as this if:

- Any of the details you give us change;

- We have been unable to confirm the information you gave us;

- Anything about you has changed at the credit reference agency when we make a full loan application search at the time you apply; or

- Following our discussion with you about your needs and circumstances, we find that we do not have a suitable mortgage for you.

We will base our Agreement in Principle on the maximum loan we think you can afford. It will not take into account the type of property you eventually buy or if you buy under certain Schemes such as Help to Buy.

Sometimes the amount we are prepared to lend may change depending on the property you choose. This is because we expect you to put down a bigger deposit on some types of properties.

Applying for an Agreement in Principle

Online

Start your application online and we'll confirm whether we’re able to give you an Agreement in Principle. Start online now

Alternatively, you can speak to us over the phone or in branch.

You may also like